Toggle navigation

Opening Balance Sheets: Indicators and Descriptions

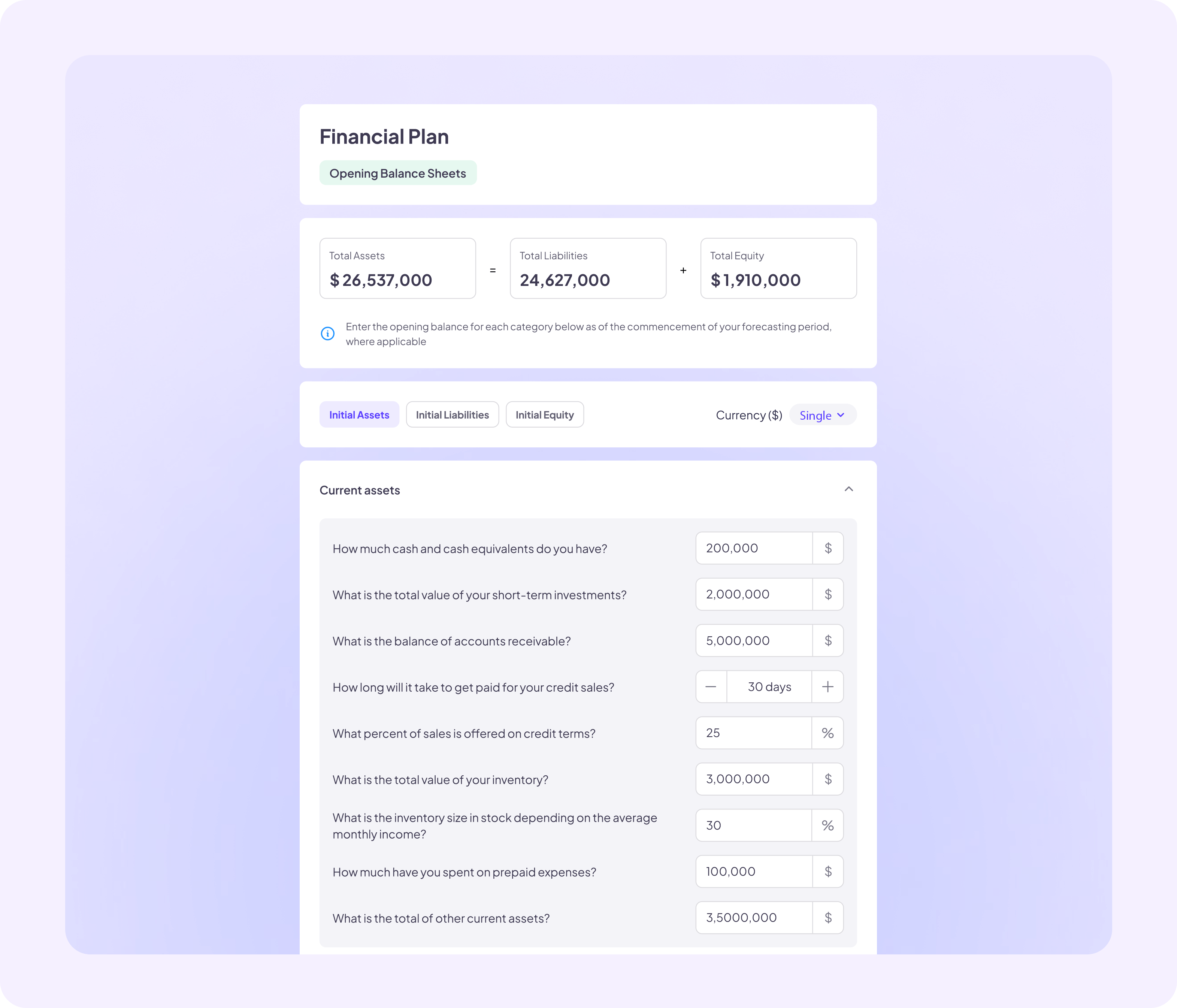

The Opening Balance Sheets section is essential for creating a financial balance that reflects your business's current assets, liabilities, and equity. This balance sheet is a key tool for investors and banks to assess your financial stability, resource efficiency, and project risks. A well-prepared balance is a crucial step toward securing funding and demonstrating the potential of your business plan.

- Total Assets: The sum of all resources owned by the company, including cash, inventory, property, and equipment.

- Total Liabilities: The total obligations the company owes, such as loans, accounts payable, and other debts.

- Total Equity: The difference between total assets and total liabilities, representing the owners' stake in the business.

Current Assets

- Cash and Cash Equivalents: Funds immediately available for operations. Reflects the company’s liquidity and financial strength.

(e.g., bank accounts, petty cash, money market funds, short-term deposits, Treasury bills) - Short-Term Investments: Investments that are easily convertible to cash within a year. Highlights asset liquidity.

(e.g., marketable securities, certificates of deposit, mutual funds, commercial paper) - Accounts Receivable: Payments owed by customers for goods or services delivered. Indicates sales efficiency and customer credit management.

(e.g., customer invoices, trade receivables, outstanding balances, credit sales) - Credit Sales Payment Terms: The duration customers take to pay for goods or services purchased on credit. Affects cash flow predictability.

(e.g., 30-day terms, extended credit terms, installment plans) - Credit Sales Percentage: The share of total sales conducted on credit terms. Impacts working capital and cash flow.

(e.g., 20%, 50% of total sales made on credit) - Inventory Value: The worth of goods available for sale. Reflects production efficiency and demand alignment.

(e.g., raw materials, work-in-progress, finished goods, consumables, spare parts) - Prepaid Expenses: Payments made in advance for future benefits. Indicates proactive financial planning.

(e.g., prepaid insurance, prepaid rent, annual software licenses, advance payments for services) - Other Current Assets: Any additional assets that can be liquidated within a year. Completes the company’s short-term asset profile.

(e.g., refundable deposits, short-term loans, prepaid taxes, current account advances)

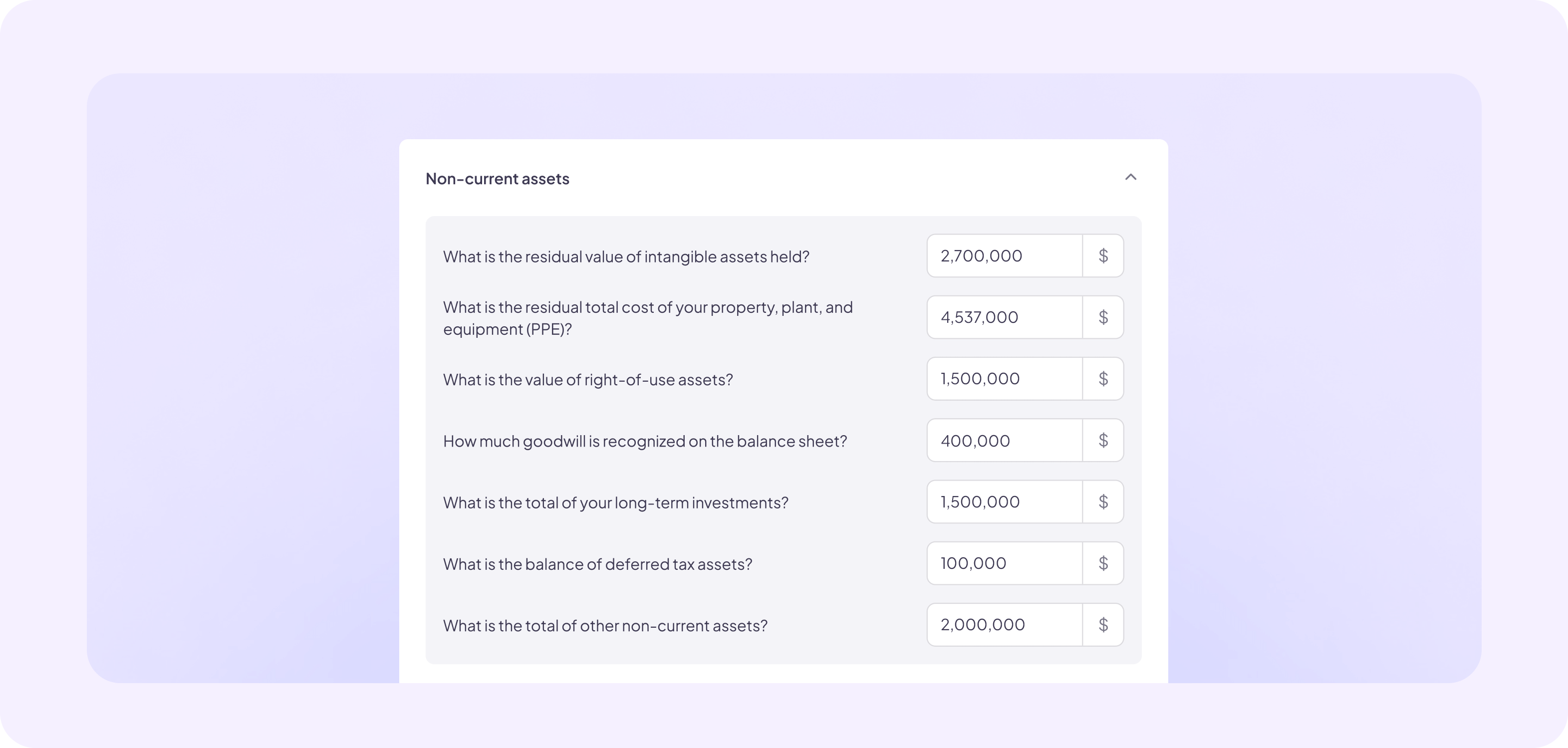

Non-Current Assets

- Intangible Asset Residual Value: Remaining value of non-physical assets like patents and trademarks. Reflects the company’s intellectual property strength.

(e.g., patents, trademarks, copyrights, goodwill, software licenses, franchises) - Total PPE (Property, Plant, and Equipment) Cost: Represents the investment in physical assets for operations. Indicates the company’s operational capacity and asset base.

(e.g., buildings, machinery, vehicles, land, furniture, leasehold improvements) - Right-of-Use Assets: Value of assets leased by the company under long-term agreements. Highlights operational efficiency and asset utilization.

(e.g., leased office spaces, vehicles under lease, equipment rentals, real estate leases) - Goodwill: The premium paid during acquisitions for intangible benefits like brand or customer loyalty. Reflects strategic growth initiatives.

(e.g., customer relationships, brand equity, reputation, acquisition synergies) - Long-Term Investments: Investments intended to generate returns over an extended period. Demonstrates strategic financial planning.

(e.g., equity stakes, real estate holdings, bonds, private equity investments) - Deferred Tax Assets: Future tax benefits from temporary differences or losses carried forward. Indicates efficient tax management.

(e.g., carry-forward losses, overpaid taxes, unutilized tax credits, temporary expense recognition differences) - Other Non-Current Assets: All remaining long-term assets that contribute to operations. Ensures comprehensive asset reporting.

(e.g., long-term receivables, construction in progress, insurance deposits, restricted cash)

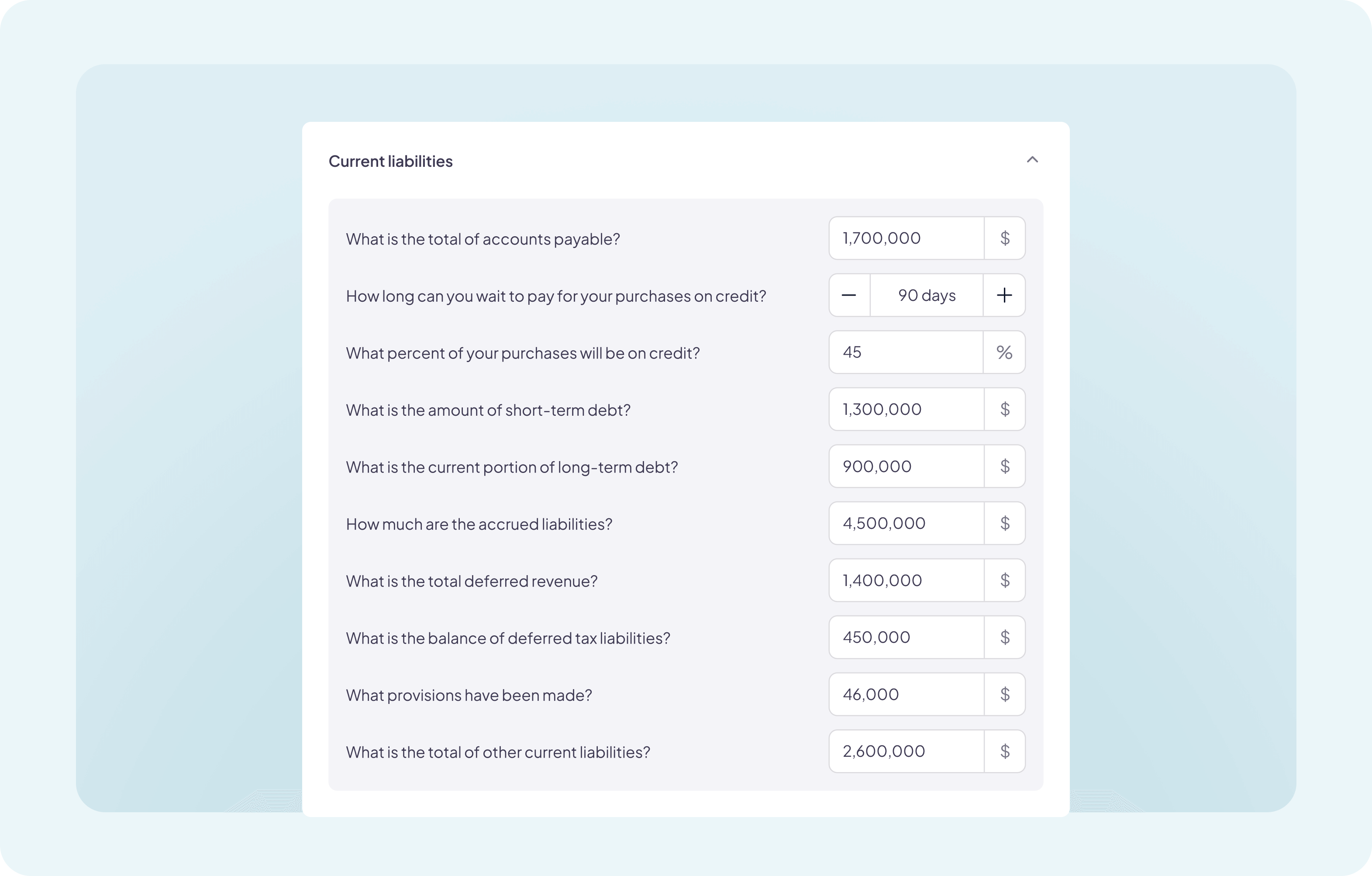

Current Liabilities

- Total Accounts Payable: Short-term debts to suppliers for goods or services. Reflects the company’s ability to meet its immediate obligations.

(e.g., trade payables, supplier invoices, utility bills, outstanding rents, accrued costs) - Credit Payment Duration: The time allowed to pay for purchases on credit, typically 30, 60, or 90 days. Affects cash flow and supplier relations.

(e.g., standard vendor terms, payment schedules, trade credit agreements) - Purchases on Credit Percentage: Proportion of total purchases made on credit terms. Indicates reliance on supplier credit for operations.

(e.g., credit purchases as % of total purchases, trade financing dependency, supplier credits) - Short-Term Debt: Loans or obligations due within one year. Assesses short-term financial stability.

(e.g., bank overdrafts, lines of credit, short-term notes payable, bridge loans) - Accrued Liabilities: Expenses incurred but not yet paid. Highlights operational efficiency and financial responsibility.

(e.g., unpaid salaries, accrued taxes, interest expenses, deferred wages, utilities payable) - Deferred Revenue: Funds received for goods or services yet to be delivered. Indicates customer trust and reliability in future operations.

(e.g., advance subscription fees, prepaid services, unearned income from projects, deposits for future deliveries) - Other Current Liabilities: Additional short-term obligations not categorized elsewhere. Ensures accurate liability accounting.

(e.g., withholding taxes, unclaimed dividends, employee benefits payable, advances from customers)

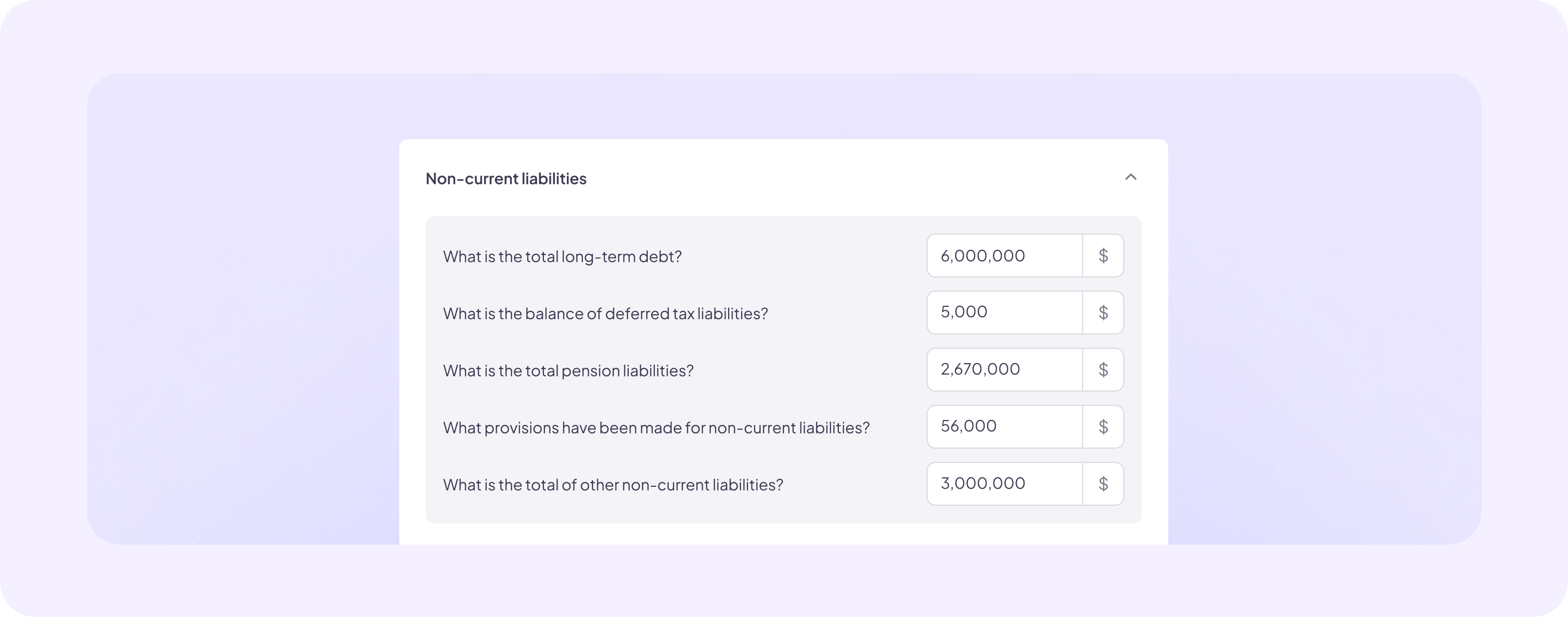

Non-Current Liabilities

- Total Long-Term Debt: Represents loans or obligations due after more than one year. Measures the company’s long-term financial commitments and leverage.

(e.g., bonds payable, mortgages, long-term loans, equipment financing, debentures) - Deferred Tax Liabilities: Taxes owed in the future due to timing differences between accounting and tax reporting. Reflects the company’s tax obligations.

(e.g., tax deferrals on depreciation, revaluation gains, undistributed earnings, amortization differences) - Pension Liabilities: Financial commitments to employee retirement plans. Indicates the company’s long-term workforce obligations.

(e.g., defined benefit plans, pension fund deficits, retirement obligations, post-employment benefits) - Provisions for Non-Current Liabilities: Amounts set aside to cover potential future obligations or risks. Highlights financial planning and preparedness.

(e.g., environmental remediation provisions, legal claims, warranty liabilities, decommissioning obligations) - Other Non-Current Liabilities: Any other long-term obligations not covered in specific categories. Provides a complete view of liabilities.

(e.g., lease liabilities, deferred revenue beyond one year, long-term deferred compensation, subordinated debt)

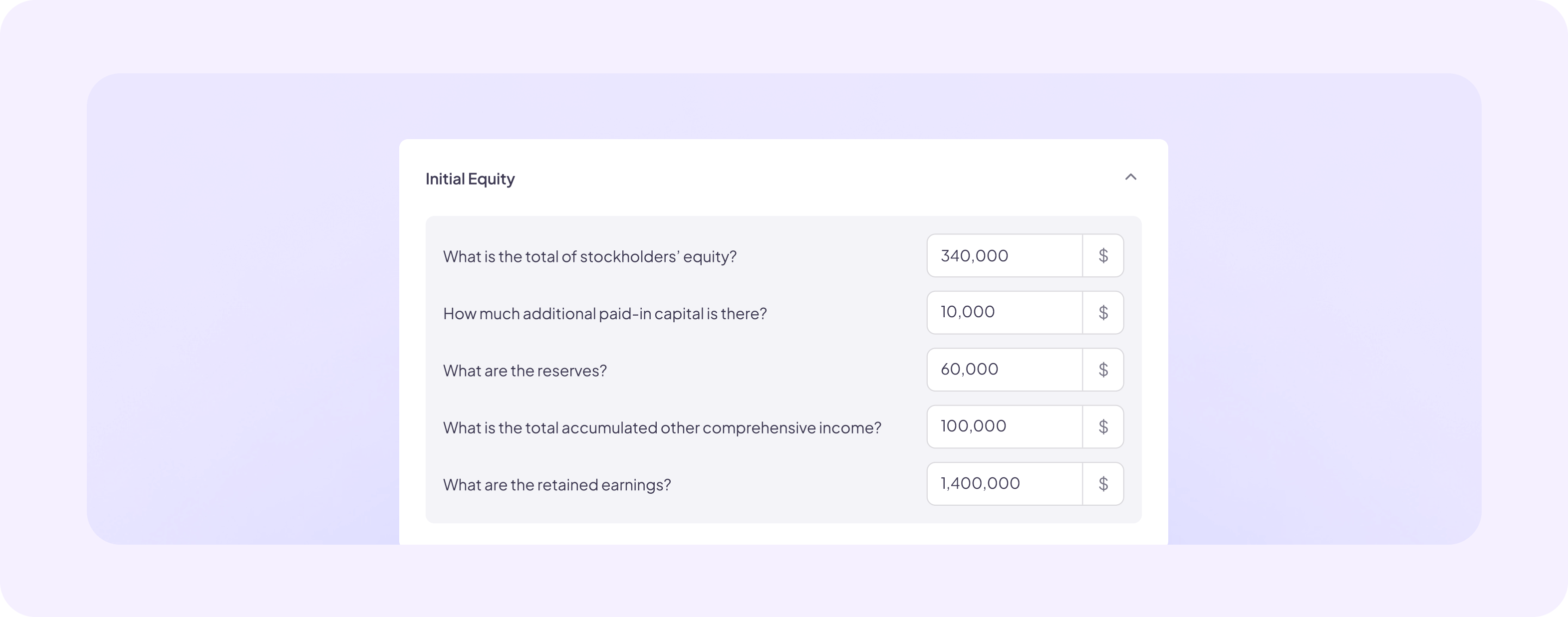

Initial Equity

- Total Stockholders' Equity: Represents the total ownership value of shareholders, including their contributions and retained earnings. Indicates the financial base and ownership structure.

(e.g., issued shares, surplus capital, capital stock, equity adjustments) - Additional Paid-in Capital: Reflects the funds received from shareholders above the nominal value of shares. Shows additional investments and company funding flexibility.

(e.g., share premium, additional shareholder contributions, excess par value, overcapitalization) - Reserves: Financial resources set aside for specific purposes such as contingencies or asset replacements. Highlights the company’s preparedness for future needs.

(e.g., general reserves, capital redemption reserves, asset replacement funds, statutory reserves) - Accumulated Other Comprehensive Income: Includes unrealized gains or losses not yet realized through operations, like currency adjustments or investments. Provides insight into external financial impacts.

(e.g., foreign currency translation adjustments, unrealized gains/losses on investments, pension adjustments, cash flow hedges) - Retained Earnings: Profits reinvested into the company rather than distributed to shareholders. Indicates growth potential and reinvestment strategy.

(e.g., unallocated profits, reinvested earnings, surplus profit balances, profit reserves)

When analyzing a balance sheet for financing decisions, banks and investors focus on key indicators of financial health. They evaluate liquidity ratios (current and quick ratios) to assess the company’s ability to meet short-term obligations, and the debt-to-equity ratio to gauge leverage and financial risk. Retained earnings and equity structure indicate profitability and reinvestment strategies, while long-term debt reveals the company’s capacity to manage financial commitments. The quality of assets—cash reserves, receivables, inventory, and fixed assets—is assessed to ensure operational continuity. A balanced, well-structured sheet with manageable liabilities and strong assets increases the likelihood of funding approval.