Toggle navigation

Opening Balance Sheets: A Foundational Guide

Why Filling in Opening Balances is Essential for Business Planning

Opening balances form the foundation for creating a forecast balance, which reflects the current financial state of the business and serves as a basis for further planning. Completing opening balances allows you to:

- Establish initial values for assets, liabilities, and equity.

- Identify financial imbalances and adjust your strategy.

- Create an accurate forecast for income, expenses, and liabilities.

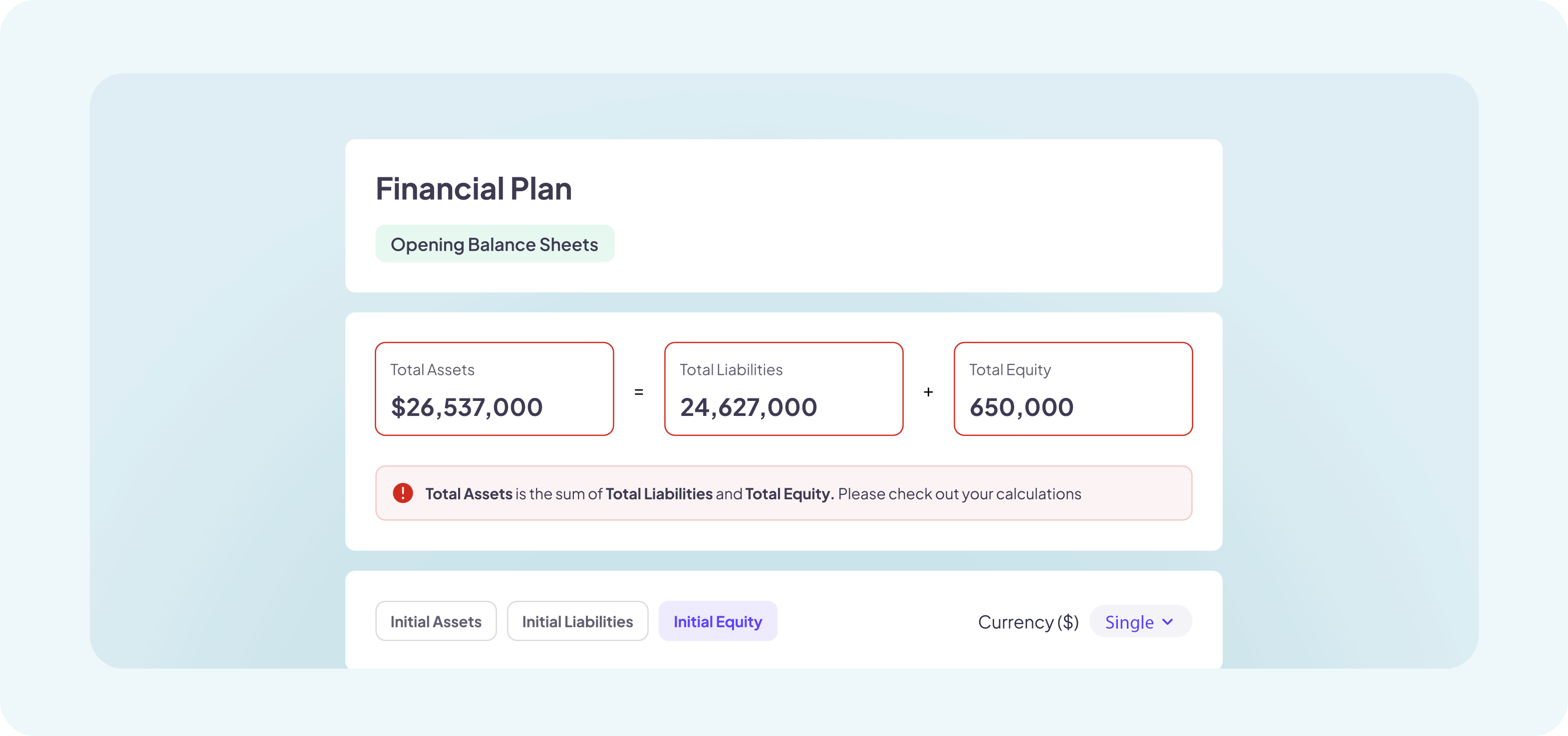

Why Assets = Liabilities + Equity Matters

The formula "Assets = Liabilities + Equity" is a fundamental principle of accounting. It helps to:

- Verify the accuracy of financial data.

- Ensure a balance between the company’s resources and their sources of funding.

- Understand the structure of capital and liabilities.

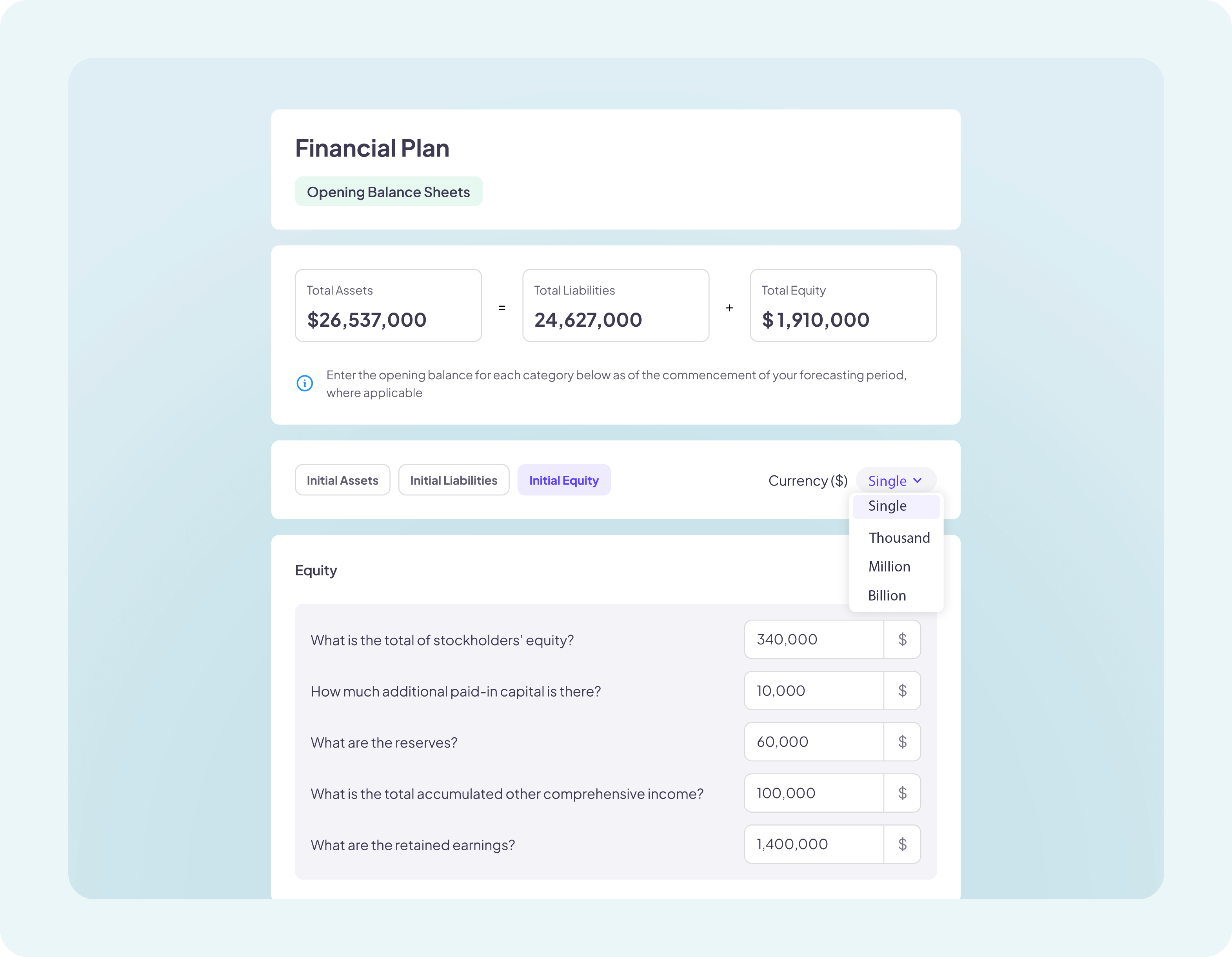

How and Why to Use the Dimension Selector

The dimension selector simplifies data input and interpretation:

- Single: Ideal for small amounts or startups with limited budgets.

- Thousand/Million/Billion: Suitable for companies with larger assets and operations.

This feature reduces visual clutter and enhances analysis accuracy.

Opening Balances for Startups vs. Mature Businesses

- Startups:

- Focus primarily on initial investments, cash, and liabilities.

- Equity mainly consists of contributions from founders.

- Mature Businesses:

- Involve more complex structures of assets and liabilities.

- Account for both long-term and short-term liabilities, accumulated capital, and depreciation.

Balance Forecasting Capabilities: Choosing Criteria

Financial planning involves forecasting based on key metrics:

Current Assets:

- How long will it take to get paid for your credit sales (30-60-90 days): Helps forecast income timelines.

- What percentage of sales is offered on credit terms (%): Determines how credit policy impacts cash flow.

- Inventory size as a percentage of average monthly income (%): Helps calculate working capital requirements.

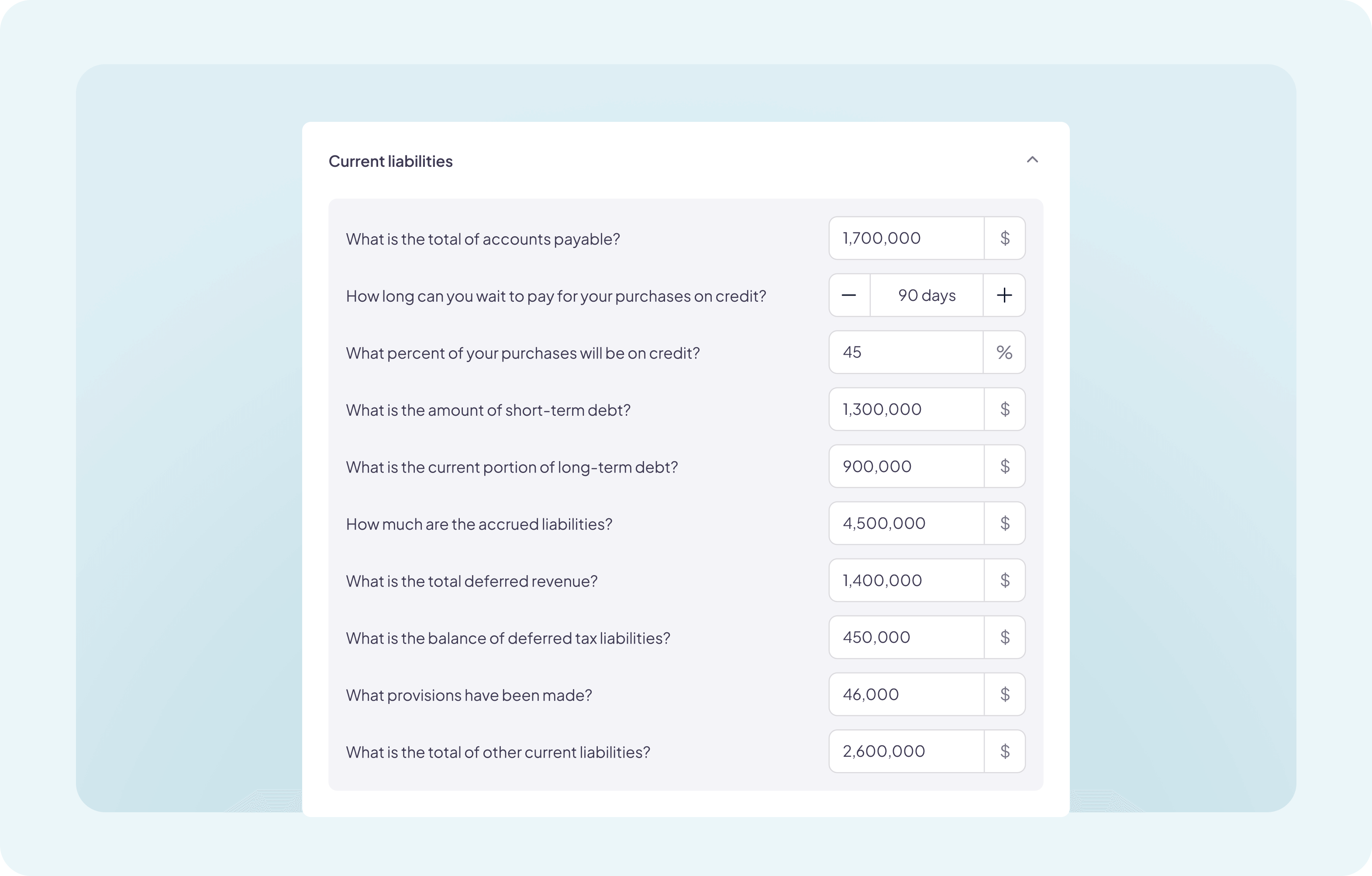

Current Liabilities:

- How long can you wait to pay for purchases on credit (30-60-90 days): Evaluates liquidity and debt management.

- What percentage of purchases will be on credit (%): Assesses the business’s debt burden.