Best US banks for small business loans

Compare lenders, understand approval requirements, and prepare your business for financing

Banks don’t approve business loans based on ideas — they approve structured, financially clear businesses.

This section helps you understand how US lending works, compare banks, and prepare everything needed for approval.

The United States offers a wide range of business lending options, from traditional commercial banks to SBA-focused lenders.

Each institution has its own requirements, loan limits, approval standards, and financing structures.

How to Choose a Bank for a Business Loan

Follow this sequence — it filters banks faster than any list.

Define how much you actually need

Start with the amount — this immediately eliminates half of your options.

- up to $100K → almost any bank or credit product will work

- $100K–$500K → focus on small business or SBA-oriented lenders

- $500K+ → only banks that handle larger commercial loans

Match the loan type to your use

Don’t compare banks yet — compare products.

- ongoing expenses → line of credit

- expansion / hiring → term loan or SBA

- equipment → equipment financing

Check real eligibility (not generic requirements)

Yes, most banks say “2+ years” — but actual thresholds vary. Look deeper:

- minimum revenue expectations

- credit score sensitivity

- collateral requirements

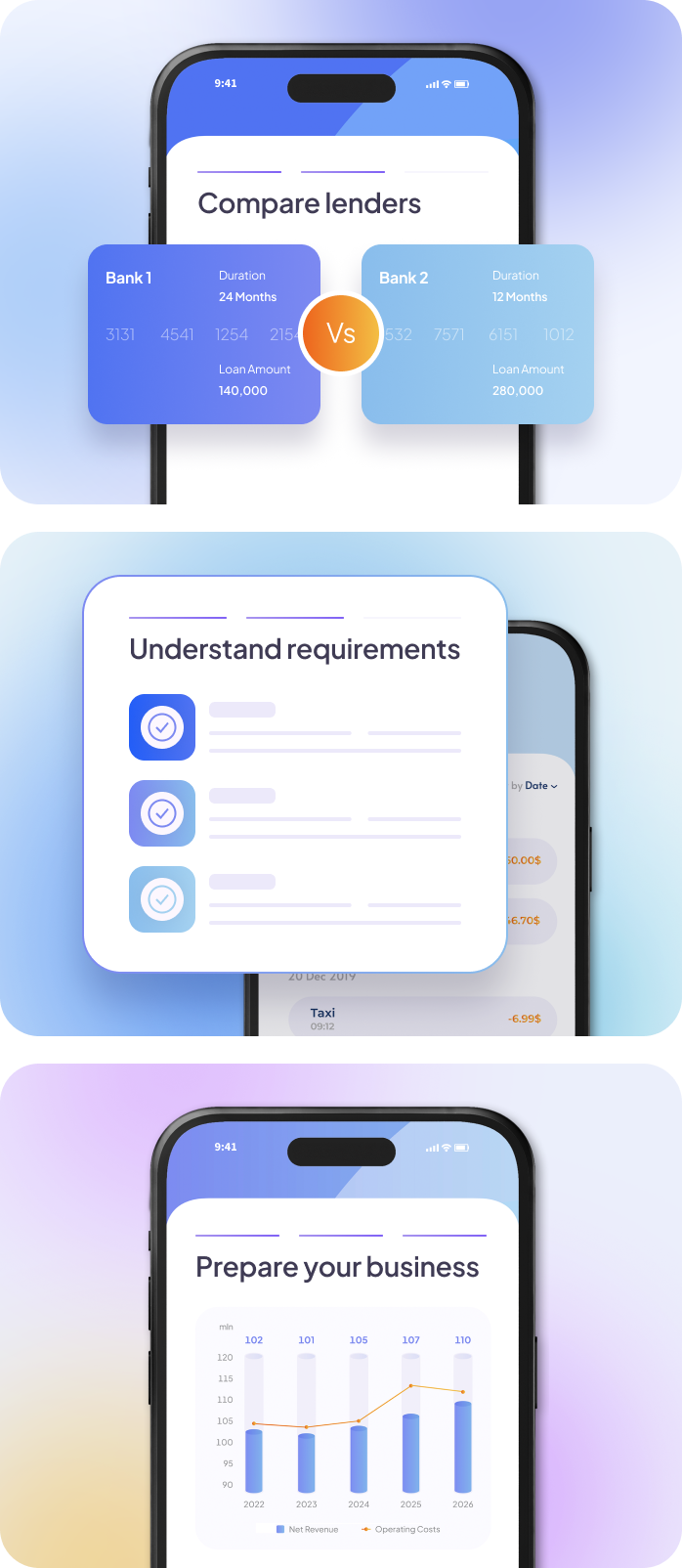

Compare total cost, not just the rate

The same “6–8%” can mean very different deals.

Look at:

- fees

- repayment structure

- term length

Evaluate speed vs. complexity

Banks differ significantly here:

- some → fast, fully online, minimal interaction

- others → relationship-based, weeks of underwriting

Narrow down to 2–3 realistic options

After applying these filters, you’re not choosing from 20 banks — but from 2–3. Compare only those:

- where you meet the requirements

- that offer the right product

- within your loan range

Lending Requirements in the USA

Business lending in the United States follows structured underwriting standards that most commercial banks apply consistently. While specific criteria vary by lender and loan program, applicants are generally expected to demonstrate financial stability, operational history, and a clear repayment strategy.

Typical requirements for U.S. business loans include:

an established operating business (often 1–2+ years)

verifiable revenue and financial records

business and personal credit review

documented purpose of the loan

ability to demonstrate repayment capacity

U.S. business registration and tax identification (EIN)

financial statements and tax returns

collateral for certain loan types

compliance with industry and regulatory standards

See How Businesses Got Approved

What mattered most: structured financial projections

What mattered most: consistency in financial records

Retail company

Retail company

What mattered most: repayment capacity

Hospitality business

Hospitality business

What mattered most: clearly defined loan purpose

Healthcare practice

Healthcare practice

What mattered most: preparation before applying

Construction company

Construction company

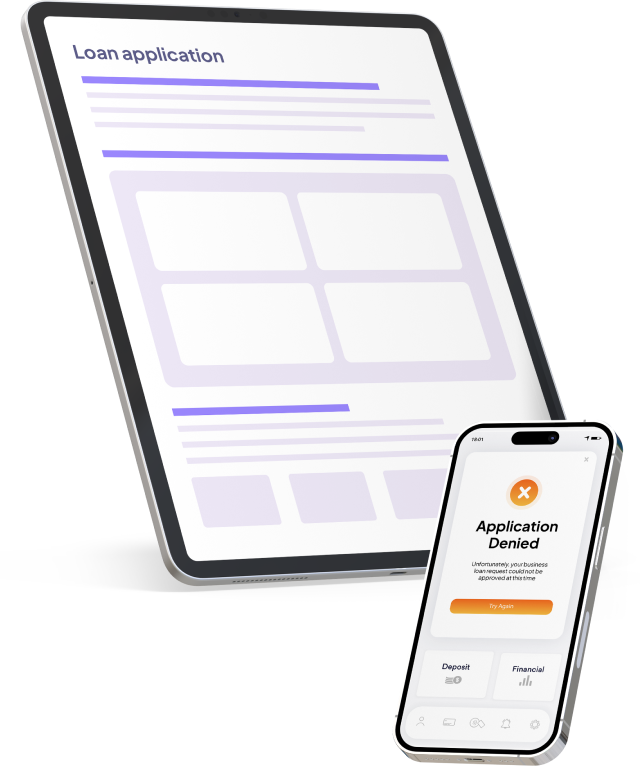

Why Business Loan Applications Get Rejected

Loan rejection is rarely about the business idea. Most applications are declined because the financial story is unclear or doesn’t meet underwriting standards.

Common reasons include:

- insufficient or unstable cash flow

- inconsistent financial statements

- short operating history

- high existing debt

- weak credit profile

- unclear loan purpose

Most of these issues are not permanent barriers — they are preparation gaps.

How to Increase Chances to Get Approved with Growexa

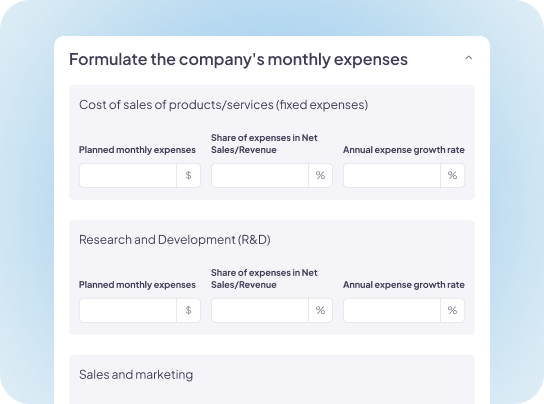

A well-structured business plan helps organize financial data, clarify how funds will be used, and demonstrate how the loan will be repaid — all of which directly address the concerns lenders evaluate during underwriting.

A clear, structured business plan helps lenders understand:

How funds will be used

How revenue will grow

How the loan will be repaid

What risks exist and how they’re managed

FAQ

Create a Bank-Ready Business Plan — Before You Apply

Plans start from $19/month

3-day free trial