Bank Credit Review Framework

How Banks Actually Decide on Business Loans

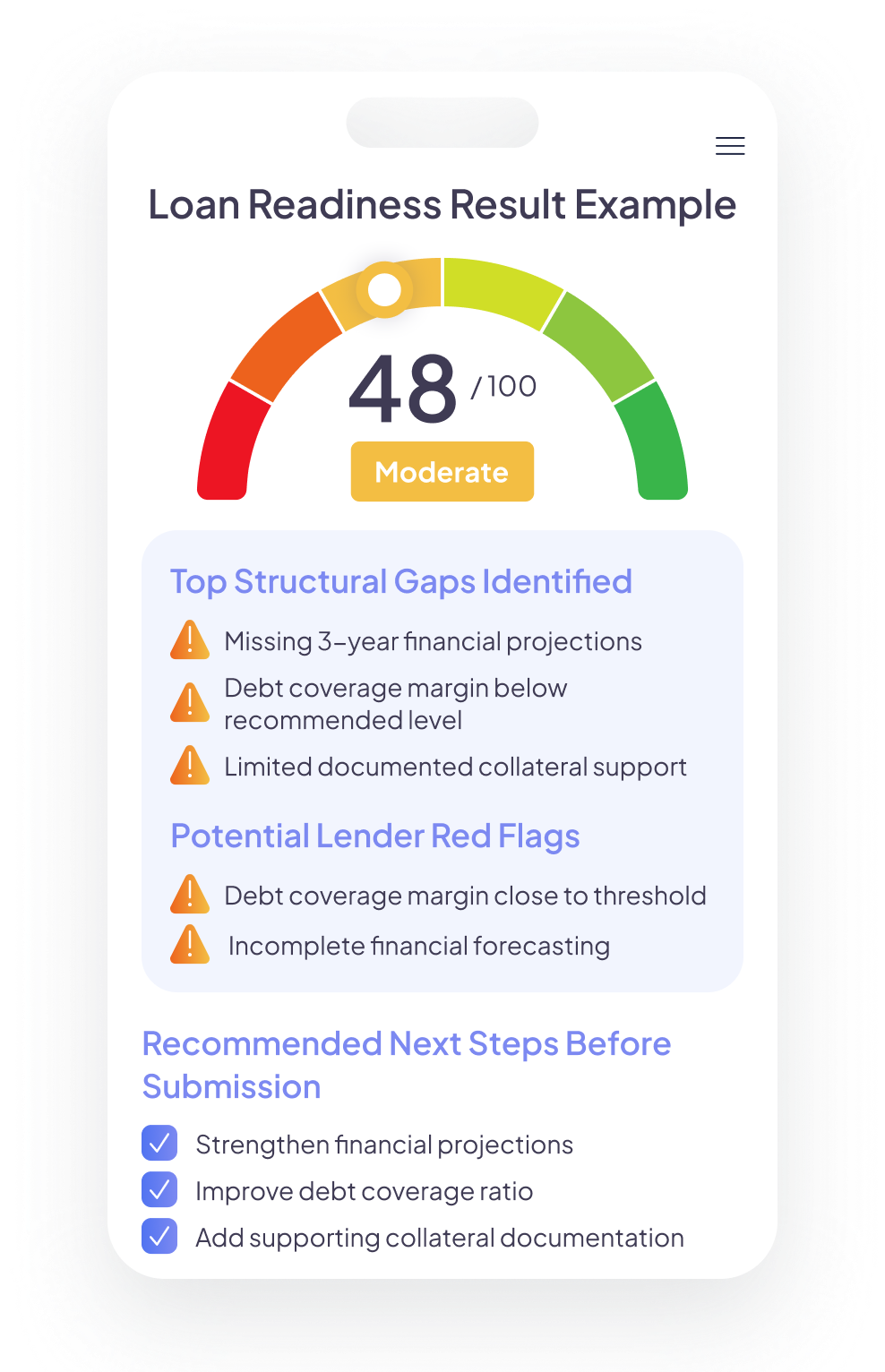

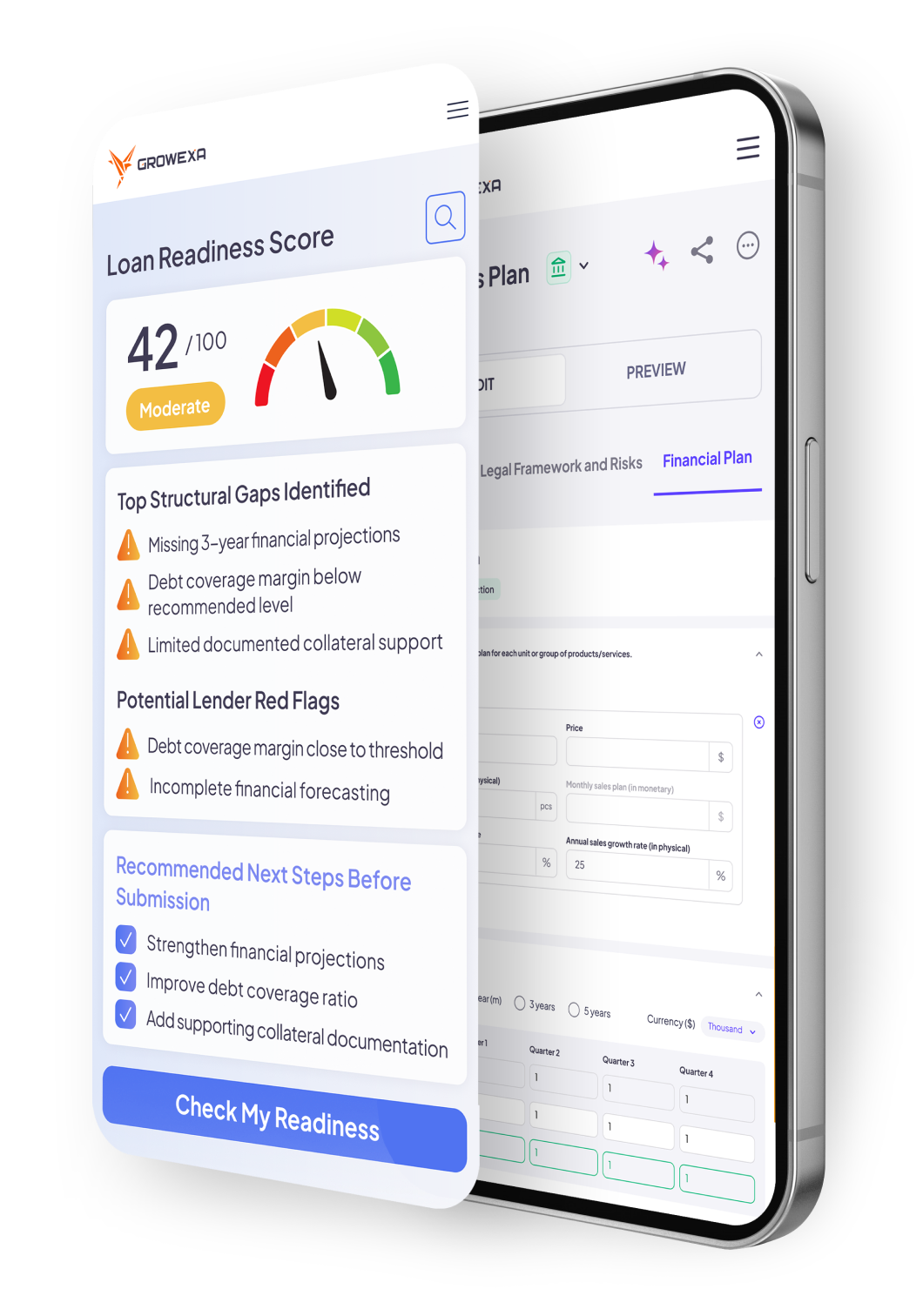

Banks don’t approve applications based on enthusiasm. They look at repayment capacity, financial consistency, documentation quality, and whether the loan structure actually fits the business.

Cash Flow & Repayment Capacity

Cash Flow & Repayment Capacity

Financial Consistency

Financial Consistency

Documentation Preparedness

Documentation Preparedness

Risk Structure & Collateral Alignment

Risk Structure & Collateral Alignment